Hyperinflation could send oil prices above $180

Published 6 Oct, 2021 08:30

As the threat of hyperinflation grows in the face of runaway government spending, growing consumer demand, and a supply chain crisis, oil prices could well hit $180 by 2022.

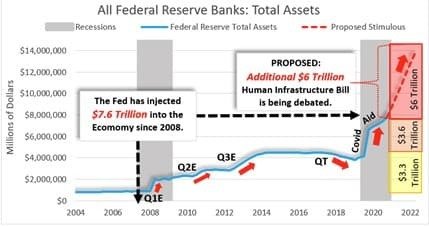

Last year, shortly after the World Health Organization (WHO) declared Covid-19 a global pandemic, governments everywhere unveiled massive monetary and fiscal stimuli (over $15T globally) in a bid to forestall the economic fallout of the pandemic. The US federal government stepped in with a broad array of measures, pumping about $4 trillion into the economy; sending cash directly to households, boosting unemployment benefits, and creating several new grant and loan programs for businesses.

It was not long before politically influential players such as Republican Senator Pat Toomey of Pennsylvania started warning of "elevated asset prices and signs of inflation" thanks to the unprecedented level of government largesse. More alarmingly, economic experts chimed in with even more dire warnings of "hyperinflation." For instance, last year, the New York Times bestselling author and founder of 'The Bear Traps Report' Lawrence 'Larry' McDonald warned of the 'cobra effect' whereby the stimuli designed to save the economy will instead "...cause a hyperinflationary economic collapse."

Also on rt.com Global thirst for oil won’t diminish until 2045, OPEC saysTrue to word, US inflation quickly shot up and has remained stubbornly high, fueled by rising consumer demand, supply chain constraints, and a commodity price boom, including the huge oil and gas rally. In August, the consumer price index or CPI rose by 5.4% on a year-over-year basis, marking the largest such increase since July 2008.

Oil prices and inflation are connected in a cause-and-effect relationship. As oil prices climb, inflation tends to follow in the same direction. On the other hand, inflation tends to fall in tandem with falling oil prices. That's the case because oil is a major input in the economy, and if input costs rise, so should the cost of end products.

Oil Prices and Inflation

President Joe Biden has lately sought to soothe fears that rising inflation could hurt the US recovery and undermine his $4-trillion spending plans. This comes after US inflation has skyrocketed even as the economy continues to recover following the Covid-19 related lockdowns.

Rising inflation is mainly being driven by demand for goods and services outpacing the ability of companies to keep up with supply-side bottlenecks hampering diverse industries, including the semiconductor and solar sectors. Significant stimulus funding, as well as a surge in the US personal savings rate, has added to this.

Republicans have already seized on the alarming inflation trend to oppose Biden's ambitious spending plans saying the country can ill-afford additional government spending proposals that might juice the economy.

Also on rt.com Russia’s oil output hits record high in SeptemberThe Biden administration will probably be feeling a little jittery about high oil and gasoline prices not only because of the role that oil has historically played in dictating inflation trends but also because of the risk they pose to his future political ambitions. It's a well-known fact that gas prices have an outsized impact on the consumer psyche.

Gas prices currently sit at an average of $3.20 per gallon nationally. While that is only about 25 cents higher than the average during the last 10 years, it's more than a full dollar higher than prices last year.

Thankfully, the oil-inflation nexus has weakened considerably since the 1980s.

For instance, during the 1990s and the Gulf War oil crisis, inflation remained stable despite crude oil prices doubling in six months to around $30 from $14. This decoupling between the two metrics became even more apparent during the 1999 to 2005 oil price rally when the annual average nominal price of oil rose to $50 from $16.50 while CPI rose by a much smaller margin to 196.80 in Dec. 2005 from 164.30 in Jan. 1999.

The price correlation between crude and gasoline has changed quite a lot over the years - in ways that do not favor the consumer. Most states have raised gas taxes, refiners face new rules that add cost and there's a shortage of drivers for the trucks that deliver gas to filling stations.

Is high inflation bullish for oil?

The relationship between high oil prices and high inflation is, therefore, not quite as simple or straightforward.

Indeed, some experts have even made a somewhat roundabout argument that high inflation and a weakening dollar will push oil prices higher and not the other way round.

Opportune LLP says the US economy is headed for pandemic-induced hyperinflation, arguing that what took five years to do with the last QE has now been duplicated in less than a year. The analysts say that with such rapid expansion of the money supply, it's only a question of when hyperinflation will hit.

The analysts say that their models currently value West Texas Intermediate (WTI) crude oil in the $90/bbl range, good for nearly 16% upside compared to current oil prices.

But here's where it gets interesting: The experts argue that given the government's insatiable appetite for spending, the dollar could be set for massive devaluation that will propel WTI prices north of $180/bbl by the end of 2022.

We are not quite sanguine about those ultra-bullish prospects for the simple reason that they would not go down well with the Biden administration.

According to petroleum analyst Patrick De Haan of GasBuddy, one-hundred-dollar oil today could get us close to the $4 per gallon mark. The $4 threshold is regarded as an unmistakable pain point for drivers, with $4.17 being the all-time high for gas prices after oil prices hit $145/bbl in the summer of 2008.

This is not lost on Republicans, who have again seized the moment and are blaming Biden for rising gas prices.

The government still has the option to sell its strategic oil reserves if the oil rally shows no signs of slowing down and if OPEC+ or even US shale producers fail to beat it to the punch, as Pimco analysts recently pointed out.

This article was originally published on Oilprice.com