‘Emotional rollercoaster’: Cypriot students protest amid bailout furor

Published 26 Mar, 2013 11:44 | Updated 26 Mar, 2013 18:52

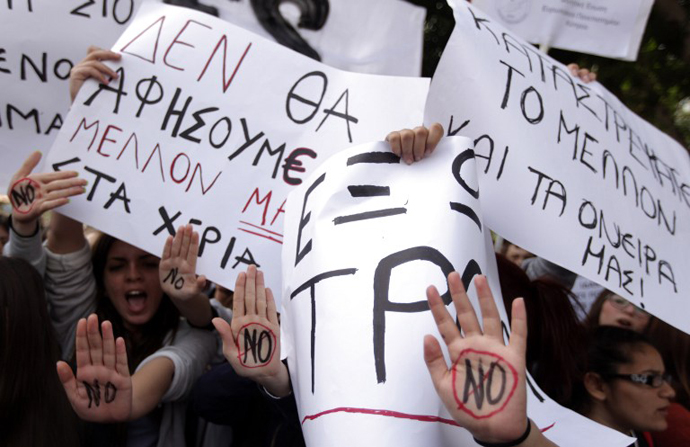

Scores of Cypriot students have flocked to the presidential palace, chanting slogans and waving banners, following the announcement that banks will not reopen until Thursday. The eurozone bailout has heightened frustration at the government.

“People wake up, they are sucking your blood,” said one

sign. “Death to Merkel,” said another.

The country’s youth are also expressing concerns about their

future: “‘Troika’ will bring us to the point that we have no

future. We cannot find a job,” a Cypriot student told RIA

Novosti.

As protesters took to the streets on Tuesday, Bank of Cyprus

Chair Andreas Artemis submitted his resignation in opposition to

plans to restructure the bank.

Unrest has widened following the $13-billion bailout deal which has

seen the freezing of deposits over €100,000. A withdrawal limit has

been imposed on ATMs, and capital controls are in place to prevent

the movement of funds.

The eurozone bailout did not alleviate the island nation's worries.

Residents who have not taken to the streets in anger are also

feeling the pinch, especially with the central bank remaining

closed. Cypriots feel that a line has been crossed, and are worried

about cash flow, jobs and savings.

Even the manager of the Bank of Cyprus, Demetris Antoniou, fears

for his employment prospects: “For the first time in my life –

for 30 years – I worried. And the last week, and especially in the

last two days. I worried a lot. It was like… I was going to wake

up, and listen to the news that I don’t have a job anymore. And I’m

50. I’m not 20. To start my life and say ‘okay.’”

“It is like they want to push us – the Bank of Cyprus – after a

few months, to collapse? I wonder – what is this? It’s not

fair,” he added.

The bailout plan has been met with widespread anger, with few residents welcoming the deal.

“They’re very frustrated,” said RT correspondent Tesa Arcilla, who is in Cyprus.

“This has really sent a very bad message to people. They’ve lost confidence, they’ve lost trust.” All Cypriot banks will remain closed until Thursday, despite an announcement late on Monday that they would reopen on Tuesday morning. The move has prompted concern that the country’s financial institutions are even lower on cash than expected.

Laiki Bank will essentially be shut down, resulting in widespread job-losses, which also prompted hundreds to protest over the past few days. Demonstrators at previous rallies wielded signs declaring that they would rather die standing than live in debt:

“We won’t [be] Germany’s slaves,” one read.

Capital controls are still in place in Cyprus, meaning that banks are able to impose restrictions on the amount of money citizens are able to take from the ATMs, or how much money they can move around.

“We have no cash. We are just… queueing behind the ATM machines, waiting to get some cash. For how long?” one resident said.

The restrictions are creating an intense atmosphere of uncertainty, and some mild hoarding of cash supplies.

“Everybody is trying to hold onto those 5 or 10 euros that they have just in case there’re even lower limits, because right now they can only take about 100 euros,” Arcilla reported.

Some are even feeling nostalgic for the old Cypriot pound.

“With the pounds – peace and quiet,” another resident said.

“It’s better to go back to the pound.”

The recent events in Cyprus have prompted fears that similar moves could be enforced in other countries, and could be a template for how problems are dealt with in the future.

“If there is a risk in a bank, our first question should be 'Okay, what are you in the bank going to do about that? What can you do to recapitalize yourself?' If the bank can't do it, then we'll talk to the shareholders and the bondholders, we'll ask them to contribute in recapitalizing the bank, and if necessary the uninsured deposit holders,” Dutch Finance Minister Jeroen Dijsselbloem told Reuters.

There is additional concern that Germany may have been trying to make an example of the country, and that a precedent has been set for potential future bailouts.

“If there’s unrest in Cyprus – it’s not Portugal. It’s not Spain, it’s not Greece – it’s not a massive country. So what Germany was actually able to do was to enforce its might on a small country in which any kind of unrest, violence or protest will be relatively contained,” said Financial Advisor Margaret Bogenrief, co-founder of ACM Partners.

“If you’ve been reading the press – they’ve been extremely upset about footing the bills for these other countries, and I think what they were saying was ‘look, just to let you guys know – we can do this,’” she concluded.